Bayesian Additive Regression Trees (BART), proposed by Chipman et al. (2010) (Reference 1), is a Bayesian “sum-of-trees” model where we use the sum of trees to model or approximate the target function ![f(x) = \mathbb{E}[Y \mid x]](https://s0.wp.com/latex.php?latex=f%28x%29+%3D+%5Cmathbb%7BE%7D%5BY+%5Cmid+x%5D&bg=ffffff&fg=333333&s=0&c=20201002)

As a Bayesian method, all we have to do is to specify the prior distribution for the parameters and the likelihood. From there, we can turn the proverbial Bayesian crank to get the posterior distribution of parameters and with it, posterior inference of any quantity we are interested in (e.g. point and estimate estimates of

Likelihood

The likelihood is easy to specify once we get definitions out of the way. Let

For a given

The likelihood for BART is

The response is the sum of

Prior specification: General comments

We need to choose priors for

Chipman et al. actually decided not to put a prior on

As for the other parameters, we introduce independence assumptions to simplify the prior specification. If

![\begin{aligned} p \left( (T_1, M_1), \dots, (T_m, M_m), \sigma \right) &= \left[ \prod_j p(T_j, M_j) \right] p(\sigma) \\ &= \left[ \prod_j p(M_j \mid T_j) p(T_j) \right] p(\sigma), \end{aligned}](https://s0.wp.com/latex.php?latex=%5Cbegin%7Baligned%7D+p+%5Cleft%28+%28T_1%2C+M_1%29%2C+%5Cdots%2C+%28T_m%2C+M_m%29%2C+%5Csigma+%5Cright%29+%26%3D+%5Cleft%5B+%5Cprod_j+p%28T_j%2C+M_j%29+%5Cright%5D+p%28%5Csigma%29+%5C%5C++%26%3D+%5Cleft%5B+%5Cprod_j+p%28M_j+%5Cmid+T_j%29+p%28T_j%29+%5Cright%5D+p%28%5Csigma%29%2C+%5Cend%7Baligned%7D&bg=ffffff&fg=333333&s=0&c=20201002)

and that

To complete the prior specification, we just need to specify the priors for

The

For

where

- Get some estimate

of

and take the residual standard deviation).

- Pick a value of

- Pick a value of

th quantile of the prior on

. Chipman et al. recommend considering

,

or

.

For users who don’t want to choose

The

The prior for a tree

- The probability that a node at depth

(the root node having depth 0) is non-terminal.

- If a node is non-terminal, the probability that the

- Once the splitting variable for a node has been chosen, a probability over the possible cut-points for this variable.

Chipman et al. suggest the following:

, where

and

are hyperparameters. Authors suggest

and

to favor small trees. With this choice, trees with 1, 2, 3, 4 and

terminal nodes have prior probability of 0.05, 0.55, 0.28, 0.09 and 0.03 respectively.

- Chipman et al. suggest the uniform distribution over the

- Given the splitting variable, Chipman et al. suggest the uniform prior on the discrete set of available splitting values for this variable.

The

For computational efficiency, Chipman et al. suggest using the conjugate normal distribution

where

![\mathbb{E}[Y \mid x]](https://s0.wp.com/latex.php?latex=%5Cmathbb%7BE%7D%5BY+%5Cmid+x%5D&bg=ffffff&fg=333333&s=0&c=20201002)

If we choose

![\mathbb{E}[Y \mid x] \in (y_{min}, y_{max})](https://s0.wp.com/latex.php?latex=%5Cmathbb%7BE%7D%5BY+%5Cmid+x%5D+%5Cin+%28y_%7Bmin%7D%2C+y_%7Bmax%7D%29&bg=ffffff&fg=333333&s=0&c=20201002)

Other notes

In theory, once we define a prior and likelihood we have a posterior. The practical question is whether we can derive this posterior or sample from it efficiently. Section 3 of the paper outlines a Bayesian backfitting MCMC algorithm that allows us to sample from the posterior distribution.

The set-up above applies for quantitative

References:

- Chipman, H. A., George, E. I., and McCulloch, R. E. (2010). BART: Bayesian additive regression trees.

- Chipman, H. A., George, E. I., and McCulloch, R. E. (1998). Bayesian CART model search.

and design matrix

and design matrix  . In an

. In an

is a second hyperparameter which is usually taken to be greater than 1. The penalty function can be written explicitly:

is a second hyperparameter which is usually taken to be greater than 1. The penalty function can be written explicitly:

and

and  . The dotted lines are the penalties’ transition points (

. The dotted lines are the penalties’ transition points ( and

and  ). The SCAD and lasso penalties are the same for

). The SCAD and lasso penalties are the same for ![\beta \in [-\lambda, \lambda]](https://s0.wp.com/latex.php?latex=%5Cbeta+%5Cin+%5B-%5Clambda%2C+%5Clambda%5D&bg=ffffff&fg=333333&s=0&c=20201002) . The SCAD and MCP penalties are constant for

. The SCAD and MCP penalties are constant for ![\beta \notin [-a \lambda, a \lambda]](https://s0.wp.com/latex.php?latex=%5Cbeta+%5Cnotin+%5B-a+%5Clambda%2C+a+%5Clambda%5D&bg=ffffff&fg=333333&s=0&c=20201002) .

.

(“selection”) and

(“selection”) and  for all

for all  (“unbiasedness”), MCP minimizes the maximum concavity

(“unbiasedness”), MCP minimizes the maximum concavity

representing

representing  observations, each consisting of

observations, each consisting of  , and

, and  is estimated as the solution to the optimization problem

is estimated as the solution to the optimization problem

is

is

factor is sometimes written as

factor is sometimes written as  : the two formulations are equivalent.)

: the two formulations are equivalent.)

is a symmetric and positive semidefinite matrix to be chosen by the user. The idea is that

is a symmetric and positive semidefinite matrix to be chosen by the user. The idea is that  reduces the structured elastic net penalty to the usual one. I would also like to point out that

reduces the structured elastic net penalty to the usual one. I would also like to point out that  -consistency of structured elastic net (Theorem 1), and determine conditions for selection consistency analogous to the

-consistency of structured elastic net (Theorem 1), and determine conditions for selection consistency analogous to the  for each feature

for each feature  ) gives structured elastic net selection consistency (Theorem 4).

) gives structured elastic net selection consistency (Theorem 4).

. The LASSO corresponds to the case where

. The LASSO corresponds to the case where  and ridge regression corresponds to the case where

and ridge regression corresponds to the case where  . We typically do not consider the case where

. We typically do not consider the case where  as it results in a non-convex minimization problem which is hard to solve for globally.

as it results in a non-convex minimization problem which is hard to solve for globally. , where

, where  is the OLS solution. This is known as soft-thresholding, where we reduce something by a fixed value (in this case

is the OLS solution. This is known as soft-thresholding, where we reduce something by a fixed value (in this case  .

. ![p'(\beta) = \lambda \left[ I(\beta \leq \lambda) + \dfrac{(a\lambda - \beta)_+}{(a-1)\lambda}I(\beta > \lambda) \right],](https://s0.wp.com/latex.php?latex=p%27%28%5Cbeta%29+%3D+%5Clambda+%5Cleft%5B+I%28%5Cbeta+%5Cleq+%5Clambda%29+%2B+%5Cdfrac%7B%28a%5Clambda+-+%5Cbeta%29_%2B%7D%7B%28a-1%29%5Clambda%7DI%28%5Cbeta+%3E+%5Clambda%29+%5Cright%5D%2C&bg=ffffff&fg=333333&s=0&c=20201002)

. This corresponds to a quadratic spline function with knots at

. This corresponds to a quadratic spline function with knots at  . Explicitly, the penalty is

. Explicitly, the penalty is

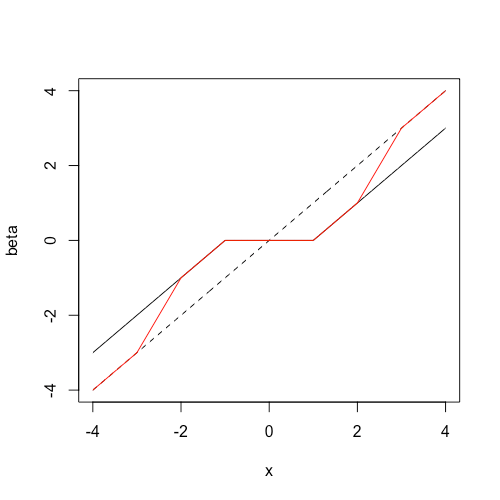

line. The line in black represents soft-thresholding (LASSO estimates) while the line in red represents the SCAD estimates. We see that the SCAD estimates are the same as soft-thresholding for

line. The line in black represents soft-thresholding (LASSO estimates) while the line in red represents the SCAD estimates. We see that the SCAD estimates are the same as soft-thresholding for  and are equal to hard-thresholding for

and are equal to hard-thresholding for  ; the estimates in the remaining regions are linear interpolations of these two regimes.

; the estimates in the remaining regions are linear interpolations of these two regimes.

, and for simplicity, assume that

, and for simplicity, assume that  and the columns of

and the columns of  . In ordinary least squares (OLS), we seek to minimize the objective function

. In ordinary least squares (OLS), we seek to minimize the objective function

. When

. When

are usually non-zero, meaning that all features need to be included in the model. Sometimes, we prefer to have the model be sparse, i.e. have the response as a function of a small subset of features only. LASSO regression (Tibshirani 1996) achieves this by replacing the sum-of-squares penalty with an

are usually non-zero, meaning that all features need to be included in the model. Sometimes, we prefer to have the model be sparse, i.e. have the response as a function of a small subset of features only. LASSO regression (Tibshirani 1996) achieves this by replacing the sum-of-squares penalty with an  penalty:

penalty:

. The “pointyness” of the

. The “pointyness” of the  , the LASSO can select at most

, the LASSO can select at most

and

and  are both tuning parameters.

are both tuning parameters.

![\phi \in (0, 1]](https://s0.wp.com/latex.php?latex=%5Cphi+%5Cin+%280%2C+1%5D&bg=ffffff&fg=333333&s=0&c=20201002) is the parameter controlling the shrinkage of the coefficients, and

is the parameter controlling the shrinkage of the coefficients, and  is the indicator function on the set of variables

is the indicator function on the set of variables  so that

so that  if

if  ,

,  otherwise. When

otherwise. When  , we obtain the LASSO solution and as

, we obtain the LASSO solution and as  , we obtain the OLS solution for the selected variables.

, we obtain the OLS solution for the selected variables. .) The adaptive lasso minimizes

.) The adaptive lasso minimizes

for some hyperparameter

for some hyperparameter  . The adaptive LASSO is selection consistent (under some assumptions).

. The adaptive LASSO is selection consistent (under some assumptions). ,

, ![\text{Annual Income } \in [\$40k, \$100k]](https://s0.wp.com/latex.php?latex=%5Ctext%7BAnnual+Income+%7D+%5Cin+%5B%5C%2440k%2C+%5C%24100k%5D&bg=ffffff&fg=333333&s=0&c=20201002) and

and  , we may want all 3 to be in the model or all 3 to be out of the model, but not just 1 of them in the model. The group LASSO (Yuan & Lin 2005) achieves this by imposing an

, we may want all 3 to be in the model or all 3 to be out of the model, but not just 1 of them in the model. The group LASSO (Yuan & Lin 2005) achieves this by imposing an  penalty on groups of coefficients. Let

penalty on groups of coefficients. Let  be a partition of

be a partition of  , i.e.

, i.e.  . The group LASSO minimizes

. The group LASSO minimizes

.

.

![\alpha \in [0,1]](https://s0.wp.com/latex.php?latex=%5Calpha+%5Cin+%5B0%2C1%5D&bg=ffffff&fg=333333&s=0&c=20201002) is a parameter.

is a parameter.